👋 Exciting news! UPI payments are now available in India! Sign up now →

Cost management in accounting - Importance, process, and strategies

Cost management is a critical aspect of accounting that helps businesses plan, control, and optimize their expenses to maximize profitability.

Whether it’s a small business or a multinational corporation, effectively managing costs ensures financial stability and efficiency. By tracking, analyzing, and adjusting expenditures, companies can make informed decisions that align with their strategic goals. This guide explores the meaning of cost management in accounting, its importance, the process involved, and the techniques businesses use to control costs effectively.

Understanding these concepts is essential for finance professionals, accountants, and business owners looking to improve operational efficiency and financial performance.

What is cost management in accounting?

Cost management in accounting refers to the process of planning and controlling a company’s expenses to improve profitability and financial efficiency. It involves identifying, analyzing, and reducing costs while maintaining the quality of goods or services. This practice is essential for budgeting, forecasting, and making strategic financial decisions.

A well-structured cost management process system enables businesses to track expenditures, allocate resources efficiently, and identify cost-saving opportunities. It includes methods such as cost estimation, cost control, and variance analysis to ensure financial stability. By implementing effective cost management techniques, companies can prevent overspending, enhance cash flow, and maintain a competitive edge in the market.

4 fundamental categories of costs

1. Fixed costs

Fixed costs are expenses that remain constant regardless of business activity levels. These costs do not fluctuate with production or sales volume. Examples include rent, salaries, insurance, and depreciation. Since fixed costs must be paid regardless of revenue generation, businesses must plan for them in their budgets. Proper management of fixed costs ensures financial stability, especially during low-revenue periods. Companies often aim to optimize fixed costs by negotiating long-term contracts or reducing unnecessary expenditures.

2. Variable costs

Variable costs change in direct proportion to production or sales levels. As output increases, these costs rise, and as production decreases, they decline. Common examples include raw materials, packaging, and commission-based salaries. Managing variable costs effectively helps businesses maintain profitability, especially in industries with fluctuating demand. Businesses often use cost-cutting techniques like bulk purchasing or process optimization to control variable costs without compromising product quality.

3. Direct costs

Direct costs are expenses that can be traced directly to a specific product, project, or department. These costs are essential for production and include raw materials, direct labor, and manufacturing supplies. Because direct costs vary depending on the number of goods or services produced, businesses must track them carefully to determine accurate pricing and profitability. Effective direct cost management helps companies improve cost efficiency and maintain competitive pricing.

4. Indirect costs

Indirect costs are expenses that are not directly tied to a specific product or service but are necessary for overall business operations. These include utilities, administrative salaries, rent for office space, and maintenance costs. Since indirect costs impact the entire organization, companies allocate them using cost allocation methods like activity-based costing (ABC). Controlling indirect costs is crucial for long-term financial health, as excessive overhead can reduce profitability.

Key elements of cost management in accounting

Cost management in accounting involves several key elements that help businesses control expenses and improve profitability. These elements include cost planning, cost reduction, and variance analysis. By implementing these practices, companies can ensure financial efficiency, allocate resources wisely, and maintain sustainable growth.

1. Cost planning

Planning is the first step of any cost management process. While planning and budgeting are two terms often used interchangeably, planning in this process refers to the research process and outlining what resources a project would need. This will give businesses a rough idea of what they will need to successfully accomplish the project, as well as what its scale would be. It also helps to break down the plan for each step of the project.

2. Cost estimation

If planning is just a rough outline, the next element of cost management in accounting is cost estimation. It’s similar to planning, but it requires a higher level of accuracy. The more accurate the estimation is to the actual costs, the better the cost management will be. Make sure that every cost is considered accurately, including fixed costs, variable costs, and any overheads. Businesses can compare the costs of past projects to get a better estimate.

3. Budgeting

The cost estimation should be developed into something more concrete. This is where budgeting comes in. One key thing about cost management in business is that it’s not enough to only know the price estimates of resources. When budgeting, make sure to consider the project scope, as well as the timeline. This allows a more concrete timeline of when the business needs to be spending the money on the resources needed.

4. Cost allocation

Other than estimated, costs should also be allocated accordingly. It’s easy for businesses to overspend when their cost breakdowns don’t specify which department or project a cost is tied to. If every cost is allocated to its appropriate department or project, businesses will be able to quickly track which departments or projects are spending the most money. Reallocating resources for better efficiency becomes a faster process, reducing the risks of overspending.

5. Cost control

Cost estimations are not always accurate. However, it’s important to still proactively compare the differences between the actual costs and the baseline estimates. When a project is in motion, make sure to monitor its spending closely and review expenses. Make adjustments to the budget as needed to ensure that the costs of the project are still within expectations. Although flexibility is important, businesses also want to instill tighter control over expenses.

6. Cost reduction

Cost reduction focuses on lowering expenses without compromising the quality of products or services. This can be achieved through process improvements, bulk purchasing, automation, and eliminating waste. Businesses often conduct regular cost audits to identify inefficiencies and implement cost-cutting measures. A well-executed cost reduction strategy enhances profitability and competitiveness while ensuring financial sustainability. However, companies must balance cost-cutting efforts to avoid negatively impacting customer satisfaction or employee productivity.

7. Variance analysis

Variance analysis is the process of comparing actual financial performance against budgeted expectations to identify discrepancies. It helps businesses understand whether they are overspending or saving in specific areas. By analyzing variances in costs, managers can take corrective actions to improve financial performance. Variance analysis is particularly useful in identifying inefficiencies, adjusting budgets, and making data-driven decisions to enhance overall cost management.

Importance of cost management in business

Cost management plays a vital role in ensuring a company’s financial health and operational efficiency. By effectively managing costs, businesses can maximize profitability, allocate resources efficiently, and maintain long-term sustainability. Below are key reasons why cost management is crucial for any organization.

Financial stability

A well-structured cost management process system ensures financial stability by preventing overspending and managing cash flow. It helps businesses handle challenges, invest in growth and innovation, and maintain relationships with stakeholders, ensuring long-term profitability and sustainability.

Budget adherence

Cost management in business helps track expenses, align spending with financial goals, and improve budget adherence. It ensures efficient fund allocation, better decision-making, and fosters accountability across departments for long-term financial success and sustainability.

Profit maximization

Effective cost management boosts profit margins by eliminating waste, optimizing efficiency, and lowering production costs. It enables reinvestment in growth, competitive pricing, and long-term profitability, while supporting employee development and market expansion for sustained business success.

Resource allocation

Effective cost management optimizes resource allocation, prioritizing high-return areas like product development, marketing, and training. It enhances efficiency, productivity, and ROI, driving growth, innovation, and competitiveness while reducing waste and strengthening internal processes for market responsiveness.

Risk mitigation

Cost management helps identify financial risks like cash flow shortages and rising costs, enabling businesses to mitigate vulnerabilities. Proactive control measures build financial reserves, diversify revenue, and ensure stability, sustainability, and resilience in uncertain economic conditions.

Performance measurement

Cost management tracks financial performance, assessing efficiency across departments and processes. It helps measure profitability, operational health, and supports goal-setting, strategic decisions, and continuous improvement by identifying inefficiencies, optimizing resources, and enhancing budget adherence for business growth.

Competitive edge

Effective cost management allows companies to offer competitive pricing without sacrificing quality, attracting more customers and strengthening market position. It also supports innovation, customer service, and long-term success by enhancing profitability and adaptability to market changes.

Informed planning decision-making

Accurate cost management data empowers leaders to make informed financial decisions, optimize planning, and align strategies with long-term goals. It helps identify cost-saving opportunities, improve forecasting, and maintain stability, driving growth and competitive advantage.

Long-term financial planning

Cost management aids long-term financial planning by forecasting expenses and revenues. Analyzing data helps businesses set growth strategies, optimize capital, and make informed investments, ensuring stability, risk mitigation, and sustained profitability in evolving markets.

Financial transparency

Clear cost records promote financial transparency, building trust with stakeholders and investors. Transparent practices reduce fraud risk, ensure compliance, and enhance credibility, fostering ethical management, responsible spending, and long-term success with stakeholder confidence.

Compliance & accountability

Cost management ensures accurate financial records, aiding compliance with regulations and tax laws. It promotes accountability, supports transparency, reduces fraud risk, and strengthens trust with investors and stakeholders, ensuring legal compliance and operational continuity.

Adaptability & flexibility

A strong cost management system helps businesses adapt to market changes and unexpected expenses. It enables financial flexibility, resource reallocation, and cost-saving measures, giving companies a competitive edge and ensuring sustainable growth and stability during economic fluctuations.

Benefits of effective cost management in a business

Effective cost management in business is essential for maintaining financial stability and ensuring business growth. By controlling expenses and optimizing resource allocation, businesses can enhance profitability, improve cash flow, and increase operational efficiency. Below are some key benefits of implementing a strong cost management strategy.

Increased profitability

One of the primary benefits of cost management is higher profitability. By reducing unnecessary expenses and optimizing spending, businesses can improve their profit margins without increasing revenue. Cost control measures, such as process optimization and waste reduction, help lower production costs and enhance overall financial performance. Increased profitability allows businesses to reinvest in growth initiatives, expand operations, and provide better returns to investors.

Better cash flow management

Effective cost management ensures that a company maintains a healthy cash flow by controlling spending and aligning expenses with revenue generation. Proper monitoring of costs helps businesses avoid liquidity issues, reduce financial strain, and ensure that they have enough funds to cover operational expenses.

By improving cash flow management, businesses can make timely payments to suppliers, employees, and creditors, reducing financial risks and improving overall stability.

Enhanced operational efficiency

Cost management in business helps streamline processes, eliminating inefficiencies that lead to unnecessary expenses. By identifying and optimizing resource usage, businesses can improve productivity while maintaining quality standards.

Implementing automation, lean management techniques, and process improvements enhances operational efficiency, reduces costs, and allows companies to focus on core business activities, leading to better overall performance.

Significant cost reduction

A structured cost management strategy helps businesses identify areas where expenses can be reduced without affecting productivity or quality. Techniques such as strategic sourcing, budget control, and supplier negotiations contribute to lowering operational and production costs.

Reduced costs enable businesses to offer competitive pricing, invest in innovation, and improve financial resilience, making them more adaptable to market fluctuations.

Improved financial reporting

Accurate cost management ensures that financial data is well-organized, making it easier for businesses to generate reliable financial reports. Proper financial reporting helps stakeholders assess a company’s performance, profitability, and financial health. With clear and transparent financial data, businesses can make informed decisions, meet regulatory requirements, and improve their credibility among investors, lenders, and regulatory authorities.

Strengthened supplier relationships

Managing costs effectively allows businesses to negotiate better terms with suppliers, ensuring cost savings and stable supply chains. By maintaining good financial health, companies can make timely payments, build trust with vendors, and secure long-term partnerships.

Strong supplier relationships lead to favorable pricing, better service levels, and improved collaboration, all of which contribute to cost efficiency and business success.

Improved stakeholder confidence

Transparent and well-managed costs instill confidence in investors, employees, and financial institutions. Stakeholders are more likely to support a business with strong financial management practices, as it indicates stability, growth potential, and lower financial risks.

Improved stakeholder confidence leads to better investment opportunities, stronger employee morale, and enhanced brand reputation, helping businesses achieve long-term success.

Enhance market position

Businesses that manage costs effectively can maintain competitive pricing while maintaining product quality and service excellence. This gives them a strategic advantage in the market, allowing them to attract more customers and increase market share.

By optimizing operational costs, companies can invest in marketing, innovation, and customer experience improvements, further strengthening their brand presence and competitiveness in the industry.

What is the process of cost management of a project?

Cost management in a project involves planning, estimating, budgeting, and controlling costs to ensure that the project stays within financial constraints. A well-structured cost management process helps businesses optimize spending, prevent budget overruns, and achieve project objectives efficiently. Below are the essential steps in managing project costs effectively.

1. Define your cost management plan

A cost management plan outlines how project costs will be estimated, budgeted, monitored, and controlled. It serves as a guideline for financial decision-making throughout the project lifecycle.

This plan should include cost estimation methods, reporting structures, approval processes, and risk mitigation strategies. Establishing a clear cost management plan ensures consistency in financial management and helps prevent unexpected cost overruns.

2. Identify key stakeholders

Stakeholders play a crucial role in cost management as they influence project funding, approvals, and financial oversight. Identifying key stakeholders—such as executives, project sponsors, finance teams, and department heads—ensures that cost-related decisions align with organizational goals.

Engaging stakeholders early in the process helps secure buy-in, define budget expectations, and maintain transparency in financial planning.

3. Set up your cost management tool

Using a cost management tool streamlines budgeting, tracking, and financial reporting. Tools like enterprise resource planning (ERP) systems, project management software, or expense tracking platforms help automate cost calculations, improve accuracy, and provide real-time financial insights.

Implementing the right tool enables businesses to monitor spending, track variances, and make data-driven financial decisions.

4. Conduct cost estimation

Cost estimation involves predicting the financial resources required for the project. This process considers labor costs, materials, equipment, overhead expenses, and potential risks.

Common cost estimation techniques include bottom-up estimating, analogous estimating, and parametric modeling. Accurate cost estimation helps businesses set realistic budgets and allocate resources efficiently to avoid financial shortfalls.

5. Develop a budget

Once cost estimates are finalized, a project budget is created to allocate funds appropriately. The budget acts as a financial blueprint, specifying spending limits for different project phases.

It includes contingency reserves to account for unforeseen costs. A well-planned budget ensures financial discipline, helps manage cash flow, and supports decision-making in case of budget deviations.

6. Set up your cost control strategy

A cost control strategy outlines how a business will monitor and manage expenses throughout the project. It includes setting cost baselines, tracking actual expenditures, and implementing approval processes for additional expenses.

Establishing a cost control framework helps prevent overspending, ensures accountability, and enables proactive financial adjustments when needed.

7. Perform variance analysis

Variance analysis compares actual project costs with the budgeted figures to identify discrepancies. This process helps project managers understand whether they are over or under budget.

By analyzing variances, businesses can pinpoint inefficiencies, detect financial risks, and take corrective actions to realign spending with the project plan.

8. Implement corrective actions

When cost variances occur, corrective actions are necessary to bring project expenses back on track. These actions may include reallocation of funds, cost-cutting measures, renegotiating supplier contracts, or optimizing resource usage.

Implementing timely corrective actions prevents financial losses and ensures project completion within the allocated budget.

9. Prepare cost reports

Regular cost reporting provides a detailed overview of financial performance, allowing stakeholders to track budget utilization. Cost reports include expense breakdowns, variance summaries, and financial forecasts.

These reports help management make informed decisions, address financial concerns, and improve cost visibility throughout the project lifecycle.

10. Communicate with stakeholders

Effective communication with stakeholders ensures transparency in financial matters and fosters accountability. Regular financial updates, budget status reports, and stakeholder meetings keep everyone informed about cost management progress.

Clear communication helps align expectations, address concerns, and ensure smooth collaboration between project teams and financial departments.

11. Evaluate change requests

Projects often encounter scope changes that impact costs. Evaluating change requests involves assessing their financial implications before approval.

Businesses must analyze whether the changes align with project goals and budget constraints. Approving unnecessary scope expansions without budget adjustments can lead to cost overruns and financial instability.

12. Adjust your budget

As projects evolve, budget adjustments may be necessary to accommodate unexpected costs or revised priorities. Adjusting the budget requires reallocating funds, securing additional resources, or optimizing existing expenditures.

Businesses should implement budget adjustments strategically to maintain financial balance while ensuring project success.

13. Conduct cost analysis

Cost analysis involves examining spending patterns, cost drivers, and financial efficiency. Businesses use this data to evaluate cost-effectiveness, identify cost-saving opportunities, and optimize resource allocation.

Regular cost analysis helps improve decision-making, enhance financial performance, and prevent unnecessary expenditures.

14. Continuous improvement

Cost management is an ongoing process that requires continuous assessment and refinement. Businesses should learn from past projects, implement best practices, and improve cost management strategies over time.

Continuous improvement helps organizations enhance financial efficiency, strengthen cost controls, and achieve long-term business sustainability.

8 effective cost management in accounting techniques

Effective cost management techniques help businesses optimize expenses, improve profitability, and maintain financial stability. By implementing strategic cost-control measures, companies can enhance operational efficiency while ensuring long-term growth. Below are eight proven cost management techniques that businesses can use to improve financial performance.

1. Activity-based costing

Activity-Based Costing (ABC) allocates costs based on specific activities that contribute to production or service delivery. Unlike traditional costing methods, ABC assigns indirect costs to products or services based on their actual consumption of resources.

This technique helps businesses identify high-cost activities, eliminate inefficiencies, and improve pricing strategies. By using ABC, companies can achieve better cost transparency, optimize resource allocation, and enhance decision-making for cost control.

2. Budgeting and forecasting

Budgeting and forecasting are essential for financial planning and cost management in accounting. A well-defined budget sets spending limits and ensures that resources are allocated efficiently. Forecasting, on the other hand, helps businesses predict future financial trends based on historical data and market conditions.

Together, these techniques enable companies to plan for potential risks, control expenses, and make informed financial decisions to maintain profitability and stability.

3. Variance analysis

Variance analysis compares actual costs with budgeted or forecasted amounts to identify discrepancies. It helps businesses understand whether they are overspending or saving in specific areas. By analyzing cost variances, companies can pinpoint inefficiencies, adjust spending patterns, and implement corrective actions.

This technique enhances financial control by ensuring that expenditures align with business objectives and identifying opportunities for cost reduction.

4. Target costing

Target costing is a proactive cost management in accounting approach where businesses set a predetermined cost for a product or service based on market conditions and customer expectations. Companies then work backward to design and manufacture the product within that cost limit.

This technique encourages cost efficiency, competitive pricing, and innovation in product development. By focusing on cost control from the beginning, businesses can maintain profitability while meeting customer demands.

5. Cost-benefit analysis

Cost-benefit analysis helps businesses evaluate the financial impact of a project, investment, or decision. It involves comparing the estimated costs against the expected benefits to determine if an initiative is financially viable.

Companies use CBA to prioritize investments, eliminate unprofitable projects, and allocate resources efficiently. By assessing potential returns, businesses can make data-driven decisions that maximize value and minimize financial risks.

6. Just-in-time inventory management

Just-in-Time (JIT) inventory management is a cost-saving technique that minimizes inventory holding costs by ordering materials and products only when needed. This approach reduces waste, storage expenses, and the risk of obsolete inventory.

By optimizing supply chain efficiency, businesses can lower costs, improve cash flow, and enhance overall operational effectiveness. JIT requires strong supplier relationships and efficient logistics to ensure timely deliveries without disruptions

7. Kaizen costing

Kaizen costing focuses on continuous cost reduction and process improvement throughout a product’s lifecycle. It encourages small, incremental changes to enhance efficiency and lower costs without compromising quality. Businesses implementing Kaizen costing involve employees at all levels in identifying cost-saving opportunities.

This technique fosters a culture of continuous improvement, leading to long-term cost efficiency, increased productivity, and competitive advantage.

8. Benchmarking

Benchmarking involves comparing a company’s cost structure and financial performance with industry standards or competitors. It helps businesses identify cost inefficiencies, best practices, and areas for improvement. By analyzing how successful companies manage their costs, businesses can adopt effective cost-control strategies and enhance competitiveness.

Benchmarking also provides valuable insights into pricing strategies, operational efficiencies, and financial sustainability.

Strategies for effective cost management

Effective cost management requires strategic planning and execution to ensure financial efficiency and profitability. Businesses can implement various strategies to control expenses, optimize resources, and improve financial performance. Below are six key strategies that help organizations manage costs effectively while maintaining operational efficiency.

Capitalize on technology

Using technology helps businesses manage costs, improve accuracy, and gain control. Tools like AI analytics, ERP software, and automation provide real-time insights, reduce errors, and improve efficiency. Cloud-based tools simplify tracking, while machine learning and RPA enhance decision-making and productivity.

Supplier management

Good supplier management ensures better prices, quality, and terms through strategic sourcing and long-term contracts. Strong supplier relationships offer discounts, better terms, and reliability, while tracking performance and collaborating can reduce costs and improve supply chain efficiency.

Cost reduction strategies

Identifying cost-cutting areas without compromising quality is essential. Businesses can reduce expenses through energy-saving, outsourcing, waste elimination, and process improvements. Bulk purchasing, better vendor contracts, and regular audits also enhance efficiency and profitability while maintaining customer satisfaction.

Lean management

Lean management reduces inefficiencies, optimizes workflows, and cuts costs by eliminating non-value-adding activities. It enhances efficiency, promotes continuous improvement, and encourages employee involvement, leading to better financial performance, agility, and cost-effective growth while improving quality and reducing production times.

Financial performance metrics

Tracking key financial metrics, like cost-to-revenue ratio, ROI, and operating expenses, helps businesses stay on budget, optimize spending, and ensure financial stability. Regular analysis boosts profitability, manages risks, and supports informed decisions for growth.

Cost monitoring systems

A cost monitoring system offers real-time insights into expenses, tracks spending patterns, and detects cost overruns. Automated tools and AI analytics improve budgeting, financial accountability, and cost control, while integration with ERP and accounting software enhances data management and financial oversight.

Manage business costs and finances in one place

Best practices for effective cost management

Effective cost management requires a strategic approach to optimize spending while maintaining operational efficiency. Businesses that follow structured cost management practices can enhance profitability, improve resource allocation, and ensure financial stability. Below are eight best practices that help organizations control expenses and maximize cost efficiency.

1. Establish clear objectives

Clear cost management objectives align financial strategies with business goals, guiding decisions on cost reduction, budgeting, and resource optimization. They help track progress, measure performance, and ensure financial stability by enabling necessary adjustments.

2. Monitor costs regularly

Regular cost monitoring helps detect budget variances, identify inefficiencies, and control overspending. Using financial dashboards and automated tools, businesses can track expenses in real-time, take proactive measures, optimize spending, and maintain financial stability and budget discipline.

3. Set up an expense management system

An expense management system automates cost tracking, improves accuracy, and gives better control over finances. It helps categorize expenses, streamline approvals, and create real-time reports. This system prevents fraud, reduces errors, ensures policy compliance, and keeps expenses within budget.

4. Encourage cross-departmental collaboration

Effective cost management involves collaboration across finance, procurement, and operations. By working together, teams can identify inefficiencies, implement cost-cutting measures, and optimize resources. This approach ensures cost-saving initiatives align with business needs and benefit the entire organization.

5. Continuously Optimize Budget Allocations

Budget reviews help businesses adapt to market changes and financial performance. Regular evaluations ensure efficient resource allocation and meeting financial goals. Quarterly or annual assessments identify spending trends, adjust projections, and enable businesses to stay financially resilient and make necessary adjustments.

6. Implement proper employee training programs

Educating employees on cost-conscious practices promotes financial responsibility. Training in budgeting, expense management, and cost-saving techniques helps employees understand the impact of their spending. Well-informed employees follow cost control measures, minimize waste, and contribute to overall cost efficiency.

7. Create Contingency Plans

Unforeseen expenses can disrupt stability, making contingency planning vital. Businesses should allocate reserve funds for emergencies or unexpected costs. A proactive approach to risk management ensures financial setbacks don’t jeopardize operations, helping maintain stability during challenging times.

8. Practice Regular Improvement

Cost management requires ongoing evaluation and refinement. Businesses should analyze performance, identify cost-saving opportunities, and improve processes. A culture of continuous improvement helps optimize spending, adapt to market changes, and enhance efficiency, ensuring long-term financial success and a competitive edge.

Difference between cost control and cost management

Cost control and cost management are essential financial practices that help businesses optimize expenses and maintain profitability. While they are related, they serve different purposes. Cost control focuses on minimizing costs within set limits, whereas cost management takes a broader approach to planning, monitoring, and optimizing costs strategically. Below are the key differences between cost control and cost management.

1. Definition

● Cost Control

Cost control involves tracking and reducing expenses to stay within budget. It includes identifying variances and taking corrective actions to prevent overspending, ensuring financial discipline and that costs don't exceed planned limits.

● Cost Management

Cost management involves planning, analyzing, and optimizing costs through budgeting, forecasting, and performance analysis. Unlike cost control, it focuses on improving financial efficiency while supporting growth and long-term sustainability.

2. Nature

● Cost Control

Cost control is reactive, focusing on fixing cost overruns after they happen. Businesses apply cost control when expenses exceed the budget, making adjustments to realign spending with goals. It’s a short-term corrective approach.

● Cost Management

Cost management involves planning, monitoring, and optimizing finances to prevent issues. It helps businesses improve efficiency, boost profitability, and ensure spending supports long-term goals.

3. Focus

● Cost control

Cost control reduces unnecessary expenses and keeps spending within budget limits, ensuring efficient resource use. Businesses apply cost control to projects, departments, or operations to maintain financial stability.

● Cost management

Cost management focuses on financial planning and resource allocation, ensuring expenditures support growth, productivity, and long-term success. It balances cost efficiency with overall business value.

4. Time Frame

● Cost control

Cost control is a short-term approach focused on reducing expenses and sticking to the budget within a project or period. Once measures are in place, attention returns to regular operations.

● Cost management

Cost management is a long-term strategy involving ongoing financial assessment and optimization. It includes forecasting costs, evaluating trends, and ensuring sustainable efficiency, leading to long-term stability and improved profitability.

5. Objective

● Cost control

Cost control aims to keep expenses within budget and reduce unnecessary spending without compromising quality. It ensures financial discipline and prevents cost overruns in businesses.

● Cost management

Cost management aims to optimize costs strategically for financial sustainability. It focuses on efficiency, resource allocation, and long-term planning, balancing cost reduction with maximizing value and profitability.

6. Techniques

● Cost control

Cost control techniques reduce expenses and ensure budget compliance. These include variance analysis, budgetary control, standard costing, and expense tracking to identify discrepancies, set limits, and minimize unnecessary spending.

● Cost management

Cost management techniques focus on improving financial efficiency. These include activity-based costing (ABC), target costing, life cycle costing, and cost-benefit analysis, which help allocate resources, design within budgets, and assess investments.

7. Example

● Cost control

A manufacturing company sets a budget for raw materials and realizes that costs are exceeding the allocated amount. To control costs, the company negotiates better prices with suppliers, reduces material waste, and implements stricter inventory control to stay within budget.

● Cost management

A tech startup is planning to expand its operations and enter a new market. Instead of simply cutting costs, the company adopts a strategic cost management approach by analyzing the most cost-effective expansion strategies, optimizing workforce allocation, and investing in automation to improve long-term financial efficiency.

Key performance indicators (KPIs) of effective cost management

Key Performance Indicators (KPIs) help businesses measure the effectiveness of their cost management strategies. These financial metrics provide insights into cost efficiency, profitability, and overall financial performance. By tracking these KPIs, businesses can make informed decisions, optimize resources, and improve financial stability. Below are some essential KPIs for effective cost management.

1. Cost variance ratio

The cost variance ratio measures the difference between actual and budgeted costs. A negative variance shows overspending, while a positive one indicates savings, helping businesses maintain financial control and improve cost predictability.

2. Cost performance index

The cost performance index (CPI) measures cost efficiency by comparing earned value to actual cost. A CPI above 1 shows efficiency, while below 1 indicates overspending, helping assess financial performance and project cost-effectiveness.

3. Budget utilization rate

The budget utilization rate measures how effectively a business uses its budget. It’s calculated by dividing actual spending by the total budget. A high rate may indicate efficient spending or a risk of overspending.

4. Return on investment

Return on investment (ROI) measures an investment's profitability relative to its cost, calculated as (Net Profit / Investment Cost) × 100. A high ROI shows strong returns, while a low ROI indicates inefficiency. Businesses use ROI to evaluate investments.

5. Gross profit margin

The gross profit margin measures profitability after deducting the cost of goods sold (COGS) from revenue, calculated as (Revenue - COGS) / Revenue × 100. A higher margin indicates better cost control and profitability.

6. Operating expense ratio

The operating expense ratio (OER) measures operating expenses as a percentage of revenue, calculated as (Operating Expenses / Revenue) × 100. A lower OER indicates better cost efficiency, while a higher OER suggests excessive spending.

7. Inventory turnover ratio

The inventory turnover ratio measures how efficiently a business sells and replenishes inventory. It is calculated as Cost of Goods Sold (COGS) / Average Inventory. A high turnover ratio indicates efficient inventory management, while a low ratio suggests overstocking or slow-moving inventory. This KPI is essential for controlling inventory costs and improving cash flow.

8. Days payable outstanding

Days payable outstanding (DPO) tracks the average time a company takes to pay suppliers, calculated as (Accounts Payable / COGS) × Number of Days. A higher DPO shows better cash flow, but too high may harm supplier relationships.

9. Overhead costs percentage

The overhead costs percentage measures indirect costs as a percentage of revenue, calculated as (Overhead Costs / Revenue) × 100. A lower percentage indicates better cost control, while a higher percentage may signal inefficiencies.

Challenges faced while implementing cost management

Implementing effective cost management can be challenging due to various internal and external factors. Businesses must navigate issues such as data accuracy, employee resistance, and market fluctuations while ensuring smooth integration with existing financial systems. Below are some of the key challenges organizations face in cost management.

Accuracy & availability of data

Cost management process depends on accurate, up-to-date financial data. Without real-time expense reports or budget forecasts, decision-making becomes difficult. Inconsistent data can lead to miscalculations and ineffective budgeting, so businesses must invest in proper data management tools and reporting procedures.

Employees’ resistance to change

Employees may resist new cost management strategies, especially if they involve automation or budget changes. To overcome this, businesses should communicate benefits, offer training, and involve employees in the process for better acceptance.

Complexity of cost structure

Large organizations face complex cost structures across departments and projects. Managing indirect, overhead, and variable costs can be overwhelming. Standardized cost accounting methods help streamline and simplify resource allocation and cost management.

Inadequate employee training

Without proper training in cost management, employees may make poor financial decisions and mismanage budgets. Regular workshops and training sessions help employees develop skills in cost control, financial analysis, and expense tracking.

Regular budget readjustments

Economic conditions, unexpected expenses, and growth require frequent budget adjustments. Without a flexible approach, businesses may struggle with long-term planning. Rolling budgets or zero-based budgeting can help maintain financial agility.

Lack of complete visibility

Lack of visibility into expenses can lead to inefficiencies and financial mismanagement. Hidden costs and fragmented reporting hinder cost control. Automated expense tracking and real-time dashboards improve transparency and help monitor spending effectively.

Changing market conditions

Market fluctuations like inflation, exchange rates, and supply chain disruptions can affect cost management. To mitigate risks, businesses should use risk management strategies, diversify suppliers, and monitor market trends regularly.

Insufficient stakeholder engagement

Cost management requires collaboration among executives, finance teams, department heads, and employees. Without active involvement, cost-saving initiatives may fail. Regular meetings, transparent reporting, and consultations ensure alignment with financial goals.

Integration with existing systems

Many businesses struggle to integrate new cost management tools with existing accounting or ERP systems, causing data discrepancies and delays. To overcome this, businesses should select tools that seamlessly integrate with their current financial systems.

Software solutions and tools for effective cost management

In today’s digital landscape, businesses rely on software solutions to streamline cost management, enhance financial accuracy, and improve efficiency. These tools help automate processes, reduce manual errors, and provide real-time insights into spending. Below are some of the most effective software solutions for cost management.

Cost management software

Cost management software helps businesses track and control expenses across departments and projects. It provides real-time insights, budget tracking, and variance analysis to improve financial efficiency. Popular tools include Oracle Primavera and SAP Project System.

ERP systems

Enterprise Resource Planning (ERP) systems integrate business processes like finance, procurement, and inventory management. Tools like SAP ERP, Oracle NetSuite, and Microsoft Dynamics help businesses streamline costs and ensure accurate financial reporting.

Budgeting and forecasting software

Budgeting and forecasting software helps businesses create financial plans, track expenses, and predict performance. Tools like Adaptive Insights, Prophix, and Vena Solutions improve budget accuracy and enable data-driven financial decisions.

Expense management software

Expense management software automates tracking, approval, and reporting of business expenses. Tools like Volopay, Expensify, and SAP Concur help control spending, ensure policy compliance, and improve financial transparency and efficiency.

Accounting software

Accounting software helps record, manage, and analyze financial transactions. Tools like QuickBooks, Xero, and FreshBooks streamline bookkeeping, automate reporting, and ensure compliance, supporting effective cost management by tracking income, expenses, and generating financial statements.

Procurement management software

Procurement management software helps businesses control purchasing costs, manage suppliers, and optimize processes. Tools like Coupa, Procurify, and SAP Ariba offer visibility into orders, contracts, and spending, reducing costs and improving vendor collaboration.

Invoice automation software

Invoice automation software digitizes invoicing, reducing errors and processing time. Tools like AvidXchange, Bill.com, and Yooz automate approvals, ensure timely payments, and prevent duplicates, improving accuracy and cash flow management.

Accounts payable software

Accounts payable (AP) software automates payment processing, helping manage vendor invoices, track due dates, and avoid late fees. Tools like Tipalti, Stampli, and MineralTree improve AP efficiency and supplier relationships.

Corporate cards

Corporate cards help businesses manage employee expenses with real-time tracking, automatic categorization, and spending limits. Solutions like Volopay, Brex, and Ramp integrate with accounting systems, improving expense reconciliation and cost visibility.

Vendor management systems

Vendor management systems (VMS) help businesses track supplier performance, negotiate contracts, and control vendor costs. Tools like GEP SMART, SAP Fieldglass, and Kissflow improve procurement workflows, compliance, and cost efficiency.

Future trends in cost management

As businesses continue to evolve, cost management is becoming more advanced with the integration of new technologies. Companies are leveraging artificial intelligence, cloud-based solutions, and blockchain to enhance financial efficiency and cost optimization. These future trends are reshaping how organizations manage expenses, improve forecasting, and ensure financial transparency. Below are some of the key trends driving the future of cost management.

1. Integration of artificial intelligence

Artificial intelligence (AI) enhances cost management by automating expense tracking, predicting trends, and identifying inefficiencies. AI tools analyze data, reduce risks, and optimize budgets, helping businesses prevent fraud and overspending while improving financial control.

2. Cloud-based solutions

Cloud-based cost management solutions are gaining popularity for their scalability and cost-effectiveness. They allow businesses to centralize data, automate reporting, and collaborate in real-time, improving flexibility, security, and compliance in cost management.

3. Data analytics & business intelligence

Advanced data analytics and business intelligence (BI) are transforming cost management by offering deeper insights into financial performance. BI tools help track financial metrics, improve budgeting, and predict future expenses, optimizing resource allocation and enhancing profitability.

4. Blockchain technology

Blockchain technology improves cost management by ensuring transparency, security, and fraud prevention. It enables real-time transaction tracking, reduces errors, and lowers transaction costs through smart contracts, enhancing auditing and compliance.

5. Predictive cost modeling

Predictive cost modeling uses historical data and machine learning to forecast future expenses, helping businesses anticipate cost fluctuations, reduce risks, and create accurate budgets for improved financial planning and sustainability.

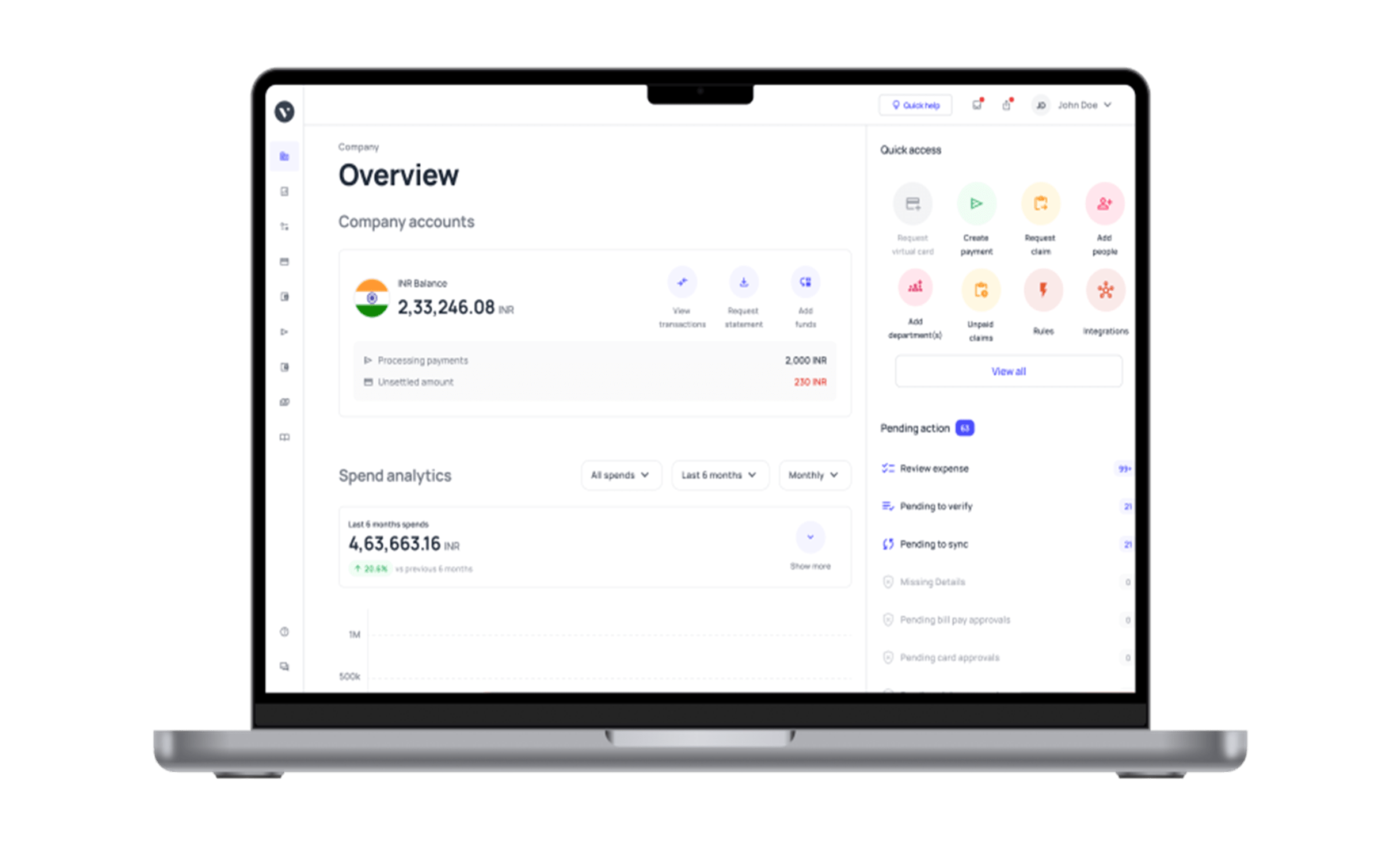

How does Volopay assist in efficient cost management for your business?

Volopay is an advanced expense management platform that helps businesses optimize costs, improve financial visibility, and automate expense-related processes. By integrating smart financial tools such as real-time tracking, automated reporting, and spending controls, Volopay ensures businesses maintain financial efficiency and accountability. Below are some key ways Volopay assists in cost management.

Real-time expense tracking

Volopay provides businesses with real-time visibility into all expenses, allowing finance teams to monitor spending as it happens. With instant notifications and transaction tracking, companies can identify unnecessary expenses and prevent budget overruns. This feature ensures that businesses maintain tighter financial control while reducing manual oversight, making expense tracking more efficient and transparent.

Automated expense reporting

Manual expense reporting is time-consuming and prone to errors. Volopay automates the entire expense reporting process, eliminating the need for manual data entry. Employees can upload receipts digitally, and the system automatically categorizes and records expenses. This automation reduces administrative workload, ensures accuracy, and speeds up the approval process, helping businesses manage costs efficiently.

Automated expense reconciliation

Reconciling business expenses with bank statements and accounting systems can be complex and tedious. Volopay simplifies this process by automatically matching expenses with corresponding transactions. This reduces reconciliation errors, minimizes discrepancies, and saves valuable time for finance teams. Automated reconciliation also ensures financial data remains accurate and up to date.

Customizable spending controls

With Volopay, businesses can implement customizable spending controls to manage budgets effectively. Admins can set spending limits for employees, departments, and vendor payments, ensuring expenses remain within budget. These controls help prevent overspending, improve financial discipline, and enhance cost accountability across the organization

Vendor management system

Managing vendor payments manually can lead to inefficiencies and late payments. Volopay offers a vendor management system that automates invoice processing and payments. Businesses can schedule payments, track due dates, and maintain a record of all vendor transactions. This streamlines procurement processes and strengthens supplier relationships while ensuring cost-effective vendor management.

Integration capabilities

Volopay seamlessly integrates with popular accounting software such as Xero, QuickBooks, and NetSuite, allowing businesses to sync financial data automatically. This integration eliminates manual data transfers, reduces accounting errors, and ensures real-time financial reporting. By connecting Volopay with existing financial systems, businesses can streamline cost management and improve workflow efficiency.

Detailed spend analytics

Effective cost management requires deep insights into spending patterns. Volopay provides businesses with detailed spend analytics, offering reports on spending trends, budget variances, and cost-saving opportunities. These analytics help finance teams make data-driven decisions, optimize budgets, and improve overall financial efficiency. By leveraging real-time data, businesses can proactively manage expenses and enhance profitability.

Automated cost allocation

Volopay simplifies cost allocation by automatically categorizing expenses based on departments, projects, or cost centers. This feature helps finance teams track where money is being spent and allocate resources efficiently. Automated cost allocation reduces manual work, improves financial reporting, and enhances budget accuracy.

Explore all-in-one cost management solution built for finance teams

FAQs on cost management in accounting

Employee engagement is key for cost management, promoting compliance, cost-conscious behavior, and proactive savings. Engaged employees reduce waste, innovate, and optimize costs, enhancing efficiency and accountability.

Scenario analysis helps businesses prepare for potential risks and opportunities by modeling different financial situations. It aids in resource allocation, contingency planning, and making informed decisions to improve financial stability and cost efficiency.

To integrate sustainability, businesses should adopt eco-friendly practices, reduce energy use, invest in green technologies, and set sustainability KPIs to align financial goals with environmental responsibility.

Cultural factors influence cost management by shaping financial attitudes, decision-making, and spending behaviors. Hierarchical cultures centralize cost control, while collaborative ones involve employees in cost-saving efforts.

In remote work environments, cost management must cover expenses like home office setups, internet reimbursements, and software subscriptions. Digital expense tracking and flexible budgeting help control costs while maintaining efficiency.

A culture of continuous improvement in cost management can be built by encouraging employee feedback, analyzing financial performance, and using technology. Regular training, recognizing cost-saving contributions, and reviewing policies ensure ongoing financial efficiency.

The long-term impact of cost management can be measured using KPIs like cost savings percentage, budget adherence, ROI, and operational efficiency. Regular audits and reviews ensure sustainable financial benefits.

Ethical cost management focuses on transparency, fairness, and compliance. It ensures cost-cutting does not harm employees, product quality, or the environment, promoting trust, brand reputation, and long-term sustainability.